What Is Multi-Ledger GHG Accounting? And Why Does It Matter for Transparency?

Companies today have more ways than ever to take meaningful action on climate change.

They can reduce emissions within their own operations. They can work with suppliers to decarbonize their value chains. They can invest in new technologies, purchase environmental attribute certificates, or otherwise support mitigation projects around the world.

Many of these actions can lead to measurable reductions, removals, or avoidance of greenhouse gas (GHG) emissions. And actions that genuinely reduce emissions should be encouraged.

But when it comes to reporting these actions – basically saying anything at all about them – things can get complicated quickly.

The Limits of Traditional GHG Accounting

For decades, corporate climate reporting has focused primarily on a company’s GHG inventory—the emissions associated with its operations and value chain.

These inventories are typically expressed through Scope 1, Scope 2, and Scope 3 emissions, which together represent the company’s attributable emissions footprint. This approach is foundational to corporate climate action. Companies need to understand where their emissions occur in order to manage them and reduce them over time.

“Inventory accounting” plays a critical role in climate strategy. It helps companies identify their largest sources of emissions, set targets, and track progress toward decarbonization.

But inventory accounting was not designed, and was never intended, to measure the full range of meaningful climate actions companies might take.

In practice, companies are increasingly investing in climate solutions that extend beyond their own operations or value chains. These actions may include financing emission reductions in other sectors, supporting nature-based removals, or investing in early-stage but critically needed decarbonization technologies.

These activities can deliver real, measurable climate benefits. Yet they are often not connected to, and not describable within, a company’s emissions inventory. Inventory accounting simply doesn’t recognize this important work.

So, this raises an important question: If these actions create climate impact—but don’t belong in a company’s emissions inventory—where should they be reported?

The Transparency Challenge

Without a clear framework to report these non-inventory actions, companies face a difficult choice.

Some organizations simply don’t report these impacts at all. Others attempt to talk about them within the context of their emissions inventory—sometimes netting operational emissions and external mitigation impacts into a single number.

Neither approach is ideal.

If companies omit these actions from their reporting, important climate investments remain invisible—and are functionally disincentivized.

But if companies mix inventory emissions and external mitigation impacts into a single metric, it’s hard to understand what has actually been done. This can create confusion for stakeholders and raise greenwashing concerns.

The reality is that these two types of information represent fundamentally different things:

A company’s emissions footprint

The climate impact of actions the company has taken

Both are important—but they should not be treated as the same metric.

Enter Multi-Ledger GHG Accounting

Multi-ledger GHG accounting offers a solution to this challenge.

Instead of trying to force all climate information into the inventory, the multi-ledger approach allows companies to report different categories of climate outcomes in separate, clearly defined ledgers.

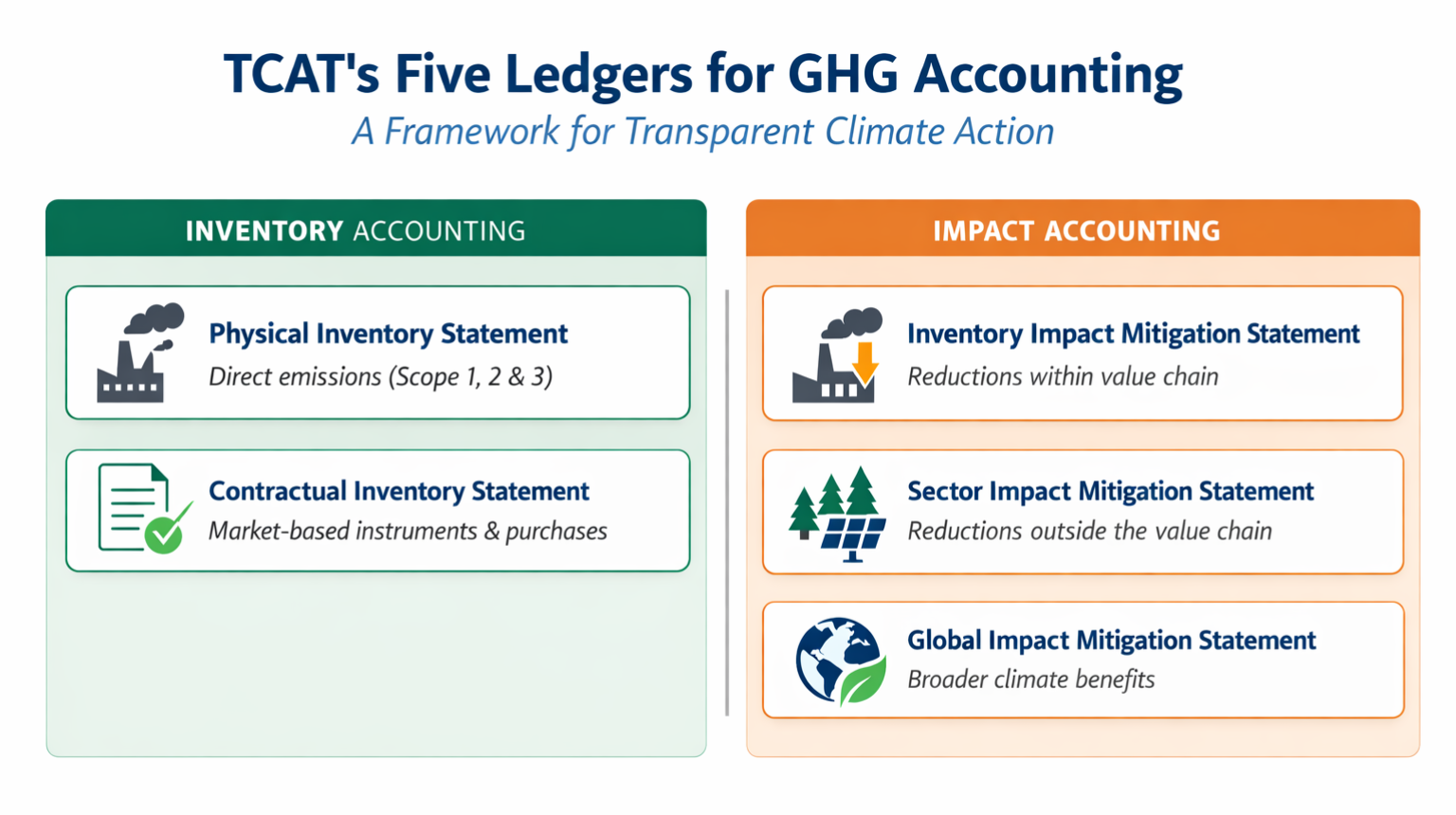

At a high level, the approach distinguishes between two complementary forms of accounting:

Inventory accounting

This measures the emissions attributable to a company’s operations and value chain—its emissions footprint.

Impact accounting

This measures the climate outcomes of mitigation actions, including those that occur outside a company’s inventory or value chain.

By separating these concepts, companies can report both sets of information transparently.

Under TCAT’s framework, this multi-statement structure allows companies to disclose their emissions footprint while also reporting mitigation outcomes across several additional statements that capture climate impacts associated with their actions.

Why Multi-Ledger Accounting Matters

Multi-ledger accounting creates several important benefits for companies and stakeholders.

1. Multi-Ledger Accounting Improves Transparency

By separating emissions inventories from mitigation impacts, companies can present a clearer picture of their climate performance.

Stakeholders can see both:

how large a company’s emissions footprint is, and

what actions the company is taking to reduce emissions within their supply chains, and beyond them. Both approaches contribute to global emissions reductions.

This clarity helps prevent misunderstandings and makes disclosures easier to interpret.

2. Multi-Ledger Accounting Encourages More Climate Action

When companies know their external mitigation investments can be transparently reported—without distorting their emissions inventory—they may be more willing to support additional climate solutions.

This creates space for companies to go beyond reducing their own emissions and contribute to broader global decarbonization.

3. Multi-Ledger Accounting Reduces Greenwashing Risk

Combining emissions reductions inside a company’s value chain with unrelated external mitigation activities in a single number can create misleading impressions.

Multi-ledger accounting prevents this by ensuring that different types of climate outcomes are disclosed separately but side-by-side.

This allows companies to communicate their full climate strategy while maintaining credibility.

4. Multi-Ledger Accounting Tells a More Complete Climate Story

Companies today are pursuing climate action in many forms: operational efficiency, renewable energy procurement, supplier engagement, technology investments, and global mitigation projects.

A company’s inventory cannot—and should not—capture all of this activity.

A multi-ledger framework allows companies to present a more accurate narrative describing how they are contributing to decarbonization—both within and beyond their value chains.

A More Transparent Way to Measure Climate Progress

As corporate climate action evolves, so must the accounting systems that measure and report its impact.

Inventory accounting will remain essential. Reducing emissions within operations and value chains is—and should remain—the foundation of corporate climate strategy.

But companies also have the potential to contribute far more broadly to global decarbonization.

Multi-ledger GHG accounting helps make those contributions visible—without compromising transparency.

By separating emissions footprints from mitigation impacts, companies can report their climate performance more clearly, reduce confusion for stakeholders, and create space for more ambitious climate action.

And ultimately, that’s the goal: not just better reporting—but better climate outcomes.